This is a speech preparation for the CIMA & AICPA Strategic Leaders Breakfast Talk, to be held in mid-February 2026, under the theme ‘Leadership in the Age of Disruption — Strategic Leadership for Modern Finance Professionals’. I will deliver the presentation from the perspective of complexity science and complexity economics, before exploring the practical implementations for management accounting professionals.

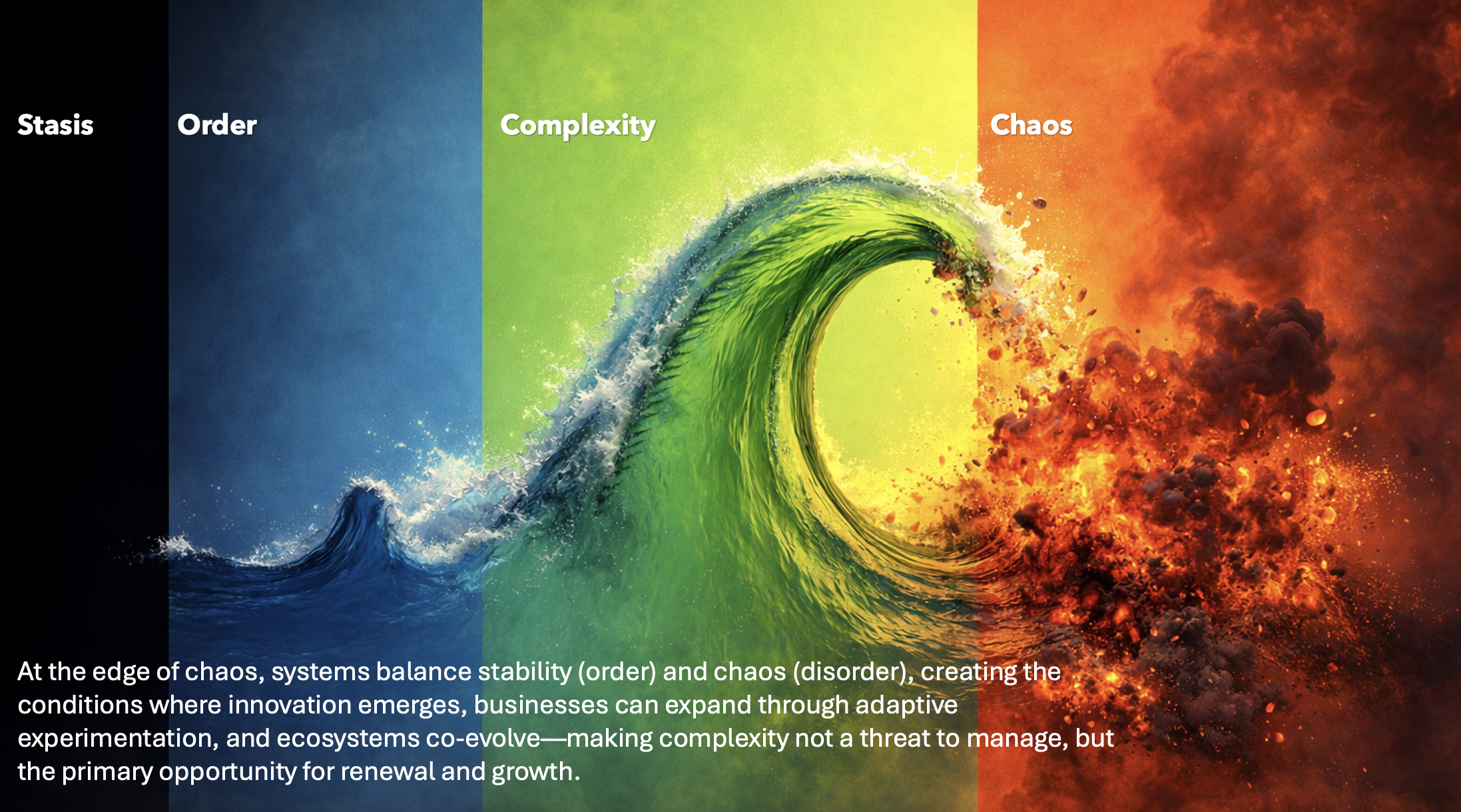

In current economic landscape, business must be perceived as the development of an ecosystem that operates as a complex adaptive system (CAS). Within this framework, autonomous agents, both internal to the firm and across broader business networks, possess the capacity for independent decision-making and activity. From this complexity perspective, phenomena such as VUCA (Volatility, Uncertainty, Complexity, and Ambiguity) and disruption are no longer viewed as external threats to be mitigated or overcome. Instead, they are recognised as engines of evolution and qualitative opportunities to redesign business architecture. Strategy shifts from the mere optimisation of saturated, linear models toward the cultivation of dynamic ecosystems that generate new value through the process of emergence.

The optimal zone for such innovation is the Edge of Chaos, which is a critical transition state where a system balances order and stability with disorder and change. It is precisely in this zone, rather than in a state of total equilibrium, where optimal innovation occurs. For the modern enterprise, the Edge of Chaos is not a threat to be avoided, but a strategic space to be occupied and, if necessary, intentionally created. Competitive advantage in this regime is defined not by scale or static efficiency, but by architectural flexibility and the velocity of learning in response to constant internal and external feedback loops.

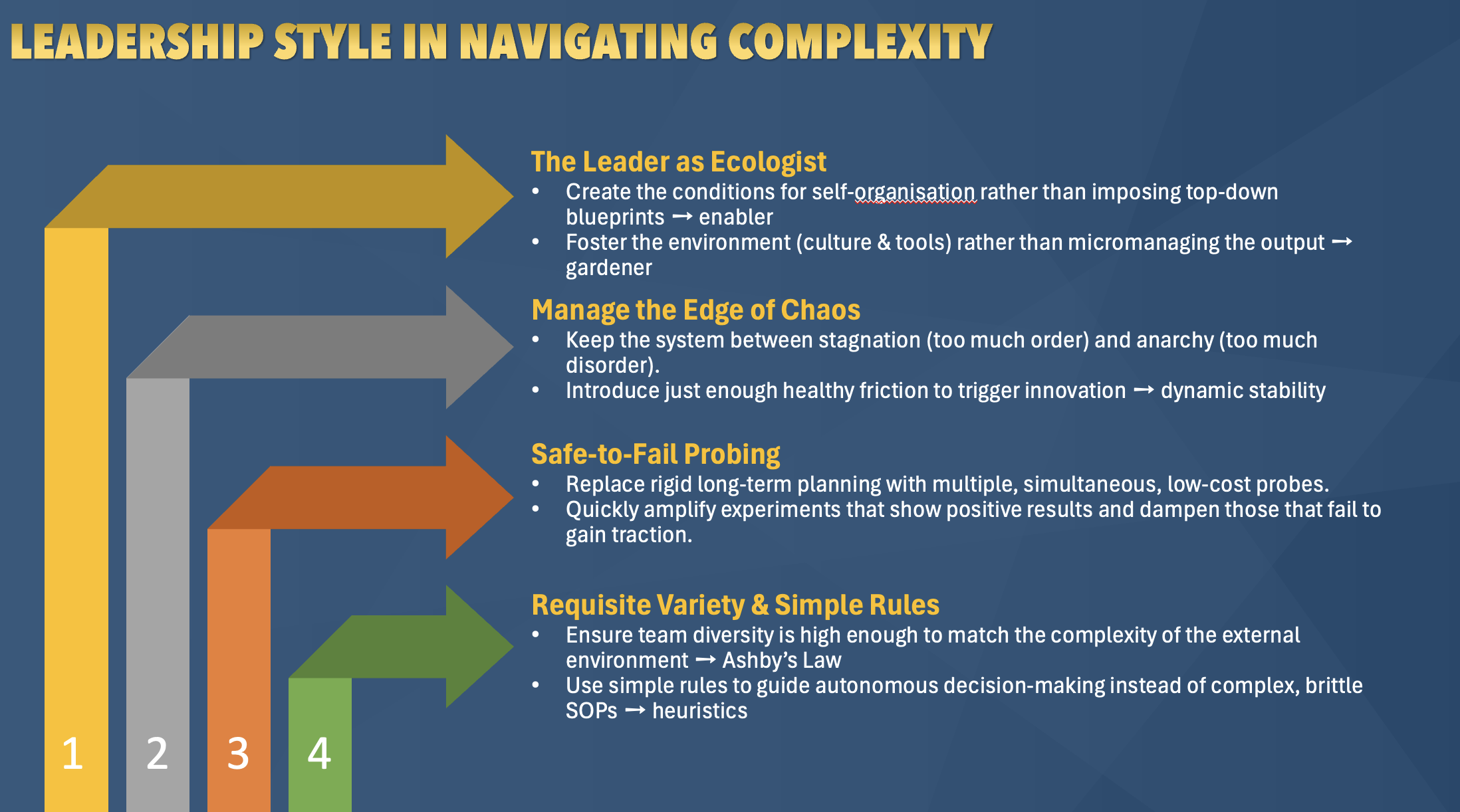

Leadership within this complex environment requires a fundamental shift in identity toward that of an ecologist. The leader’s primary duty is no longer the top-down control of outputs, but the creation of conditions and cultures that enable teams to self-organise. This involves managing the delicate tension at the Edge of Chaos, introducing enough healthy friction to trigger innovation without descending into systemic anarchy. Rigid & brittle SOPs are replaced by simple rules or heuristics that guide autonomous decision-making amidst ambiguity. Leaders must facilitate safe-to-fail probing, i.e. launching multiple, simultaneous, low-cost experiments to detect strategic signals and opportunities that traditional analytical models inevitably miss.

Strategic management in the exponential era demands ambidextrous design, balancing the exploitation of core operations with the continuous exploration of new ventures through modular structures. This necessitates the orchestration of resources far beyond traditional organisational boundaries, incorporating partners, start-ups, and regulators into platform-based strategies. Strategy is viewed as a process of co-evolution, where the organisation constantly reinvents itself to remain congruent with a shifting environment.

Finally, Management Accounting (MA) serves as the vital navigation instrument in this journey through the Strategic Planning for Exponential Era (SPX) framework. MA must evolve to support dynamic feasibility, utilising Real Options Analysis to value investments as strategic options—the right to expand, delay, or pivot—rather than rigid, one-way capital bets. This implementation includes Agile Capital Budgeting, where funds are allocated to strategic “buckets” rather than granular, unproven projects. By abandoning the stagnation of rigid annual budgets in favour of Rolling Forecasts and Throughput Accounting, MA ensures that resource allocation is driven by real-time feedback and the velocity of value conversion. Ultimately, the most profound business developments are market-creating innovations that not only ensure sustainability but actively uplift the economy and quality of life for society